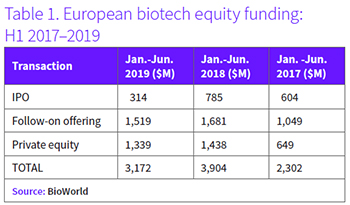

DUBLIN – European biotechnology firms engaged in drug discovery and development raised an aggregate $3.172 billion in equity investment during the first half of 2019, down 19% on the same period last year. Unless there is a substantial pickup in the third and fourth quarters, the sector's record-breaking 2018 total of $7.715 billion looks to be out of reach. (See Table 1, right.)

At the same time, the sector is still on track for a very good year, notwithstanding a marked decline in IPO funding. The total reached so far this year – $314 million spread across just four transactions – is well down on the past two years. Europe is – so far – not a major participant in what could be another record year for new biotechnology offerings on Nasdaq. (See BioWorld, May 28, 2019.)

At the same time, the sector is still on track for a very good year, notwithstanding a marked decline in IPO funding. The total reached so far this year – $314 million spread across just four transactions – is well down on the past two years. Europe is – so far – not a major participant in what could be another record year for new biotechnology offerings on Nasdaq. (See BioWorld, May 28, 2019.)

Just three European biotech firms have so far listed on Nasdaq this year: Paris-based NASH drug developer Genfit SA, which raised $145 million; Vienna (and latterly New York)-based immunotherapy developer Hookipa Pharma Inc., which took in $84 million (on top of a $37 million venture capital round in February); and Cambridge, U.K.-based oncology specialist Bicycle Therapeutics Inc., which raised $61 million.

In European markets, the trickle of IPOs is even thinner. So far, just one new offering has been completed, that of Malmö Sweden-based oncology drug developer Ascelia Pharma AB, which raised $24 million on Nasdaq Stockholm. Of course, just one big transaction could dramatically change the picture – and one such transaction is already lined up. In May, Copenhagen-based antibody developer Genmab A/S, which has long been listed on its home exchange, filed a registration statement to raise $500 million on Nasdaq. As yet, no information about the timing of the transaction has been forthcoming. Even by Nasdaq's terms, it is a big-ticket deal, but Genmab is one of Europe's biggest success stories in biotech. Barring wider macroeconomic events, it would be a major surprise if the IPO were to unravel at this point.

Follow-on offerings and private venture capital deals during the last six months are both down on the same period last year but not by such large percentages. Among listed firms, Ascendis Pharma A/S leads the way, with a mammoth $575 million in gross proceeds to fund the development and rollout of its once-weekly Transcon human growth hormone. It has already delivered in phase III trials – demonstrating superior performance to the incumbent once-per-day formulation. A BLA filing is lined up for the first half of 2020. The same company also topped the table at the midway point last year, with a $259 million stock offering, although by the end of the year that was just the sixth largest such transaction. Nasdaq has offered a good home to the Copenhagen-based company since it priced its IPO at $18 per share in 2015. The stock (NASDAQ:ASND) is currently trading close to all-time highs of over $114, and the company is valued at more than $5.4 billion.

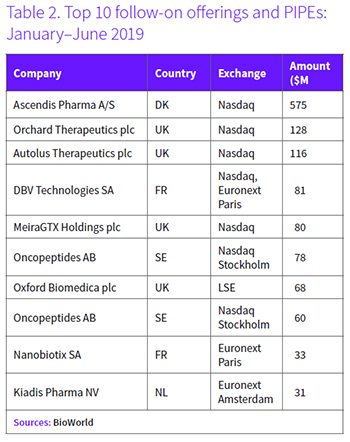

European markets featured more prominently in the top 10 follow-on offerings logged from January to June. Although the three largest transactions were all on Nasdaq, five occurred exclusively on European exchanges and one was jointly transacted between Nasdaq and Euronext Paris. (See Table 2, right)

European markets featured more prominently in the top 10 follow-on offerings logged from January to June. Although the three largest transactions were all on Nasdaq, five occurred exclusively on European exchanges and one was jointly transacted between Nasdaq and Euronext Paris. (See Table 2, right)

Swedish oncology drug developer Oncopeptides AB, of Stockholm, was actually the second highest earner during the period, chalking up two separate capital increases, of $78 million and $60 million, on Nasdaq Stockholm.

Private funding

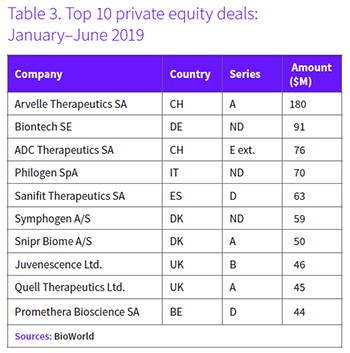

On the private equity front, the picture is – again – complicated by the Axovant stable. Although notionally headquartered in Switzerland, the firms are operationally U.S. ventures. The latest Axovant-related initiative does not carry the 'vant suffix. Arvelle Therapeutics Gmbh, which is based around the small-molecule business of the former Axovant Sciences organization, describes itself as a "European-focused biopharmaceutical company." Its $180 million series A round was led by Amsterdam-based LSP, although the syndicate was global in its reach. Arvelle is taking forward in Europe an epilepsy drug, cenobamate, which was originally discovered and developed by Seoul-based SK Biopharmaceuticals Co. Ltd. The FDA has already accepted an NDA filing. Arvelle has handed over $100 million to its partner to gain European rights to the asset and could pay up to $430 million more in regulatory and commercial milestones.

Immuno-oncology firm Biontech SE, of Mainz, is Germany's sole representative in the top 10 private equity deals, having received an €80 million strategic investment from Paris-based Sanofi SA. (See Table 3, right.)

Immuno-oncology firm Biontech SE, of Mainz, is Germany's sole representative in the top 10 private equity deals, having received an €80 million strategic investment from Paris-based Sanofi SA. (See Table 3, right.)

On the private equity front, only one other sizeable transaction was completed in Germany during the first half of 2019, a $43 million series B round at Berlin-based Atai Life Sciences AG, which is using big data to repurpose established drugs for mental health disorders.

In contrast, five firms in Belgium closed venture capital rounds above $20 million, all but one of which were above $30 million. In addition to Promethera Bioscience SA, these included Confo Therapeutics NV ($34 million), Eyed Pharma SA ($31 million), Imcyse SA ($31 million) and Agomab Therapeutics NV ($24 million). In Switzerland, four firms closed VC rounds above the $20 million bar – in addition to Arvelle, those included ADC Therapeutics SA ($76 million), Anaveon AG ($35 million) and Polyneuron Pharmaceuticals SA ($23 million). So, too, did another four in the U.K. – Juvenescence Ltd. ($46 million), Quell Therapeutics Ltd. ($44.5 million), Exscientia Ltd. ($26 million) and Wren Therapeutics Ltd. ($23 million).

Germany's lack of venture capital for biotech continues to be a fixed condition of the industry, notwithstanding the continued success of its flagship firms.