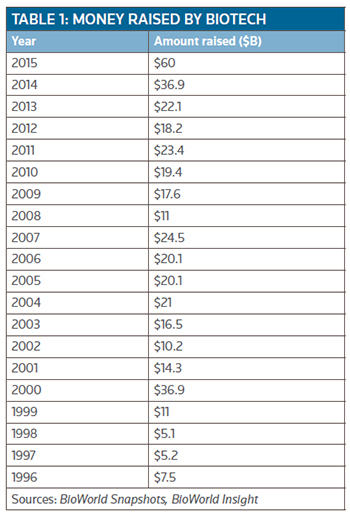

In 2014, the industry tied a longstanding 2000 record total of $36.9 billion raised from public and private financings. At the time, that amount was thought to be a hard act to follow, let alone beat. (See BioWorld Insight, Jan. 12, 2015.)

Well, records are meant to be broken, and it didn't take long to not only beat that 2014 record but literally shatter it, with 2015 financings reaching a massive total of $68.4 billion. (See Table 1, right.)

Well, records are meant to be broken, and it didn't take long to not only beat that 2014 record but literally shatter it, with 2015 financings reaching a massive total of $68.4 billion. (See Table 1, right.)

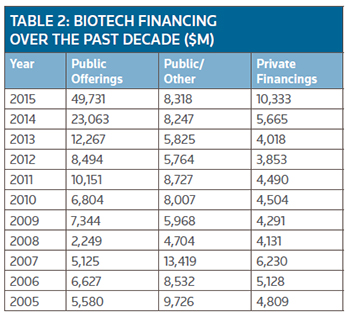

Throughout the year, public and private biotech companies appeared to have no difficulty raising cash despite the horrendous performance of the capital markets during the third and fourth quarters. The almost $50 billion raised from public offerings, including follow-ons and IPOs, was 91 percent greater than the total raised in 2014 for that category of financing, an amount that represents the highest ever raised in the history of the industry. Table 2 (below) shows just how the public offerings total in 2015 dwarfed those for the past decade. In 2000, the amount raised from public offerings was $14.7 billion.

And most of that total – approximately 70 percent of the cash generated in 2015 – came as a result of public offerings.

GIANT OFFERINGS

Serving to boost that amount were giant-sized public offerings of debt completed by Gilead Sciences Inc., Celgene Corp. and Biogen Inc. in the third quarter.

In September, Gilead priced six tranches of senior unsecured notes totaling $10 billion that it said will be deployed for general corporate purposes, such as the repayment of debt, working capital, payment of dividends and the repurchase of its outstanding common stock.

Celgene priced five series of senior unsecured notes that generated $8 billion, which the company said it will use to finance a portion of its $7.2 billion acquisition of Receptos Inc. (See BioWorld Today, July 16, 2015.)

Biogen priced a series of four senior unsecured notes for an aggregate principal amount of $6 billion, which will be used, together with cash on hand, to fund share repurchases of its common stock under the company's previously authorized $5 billion share repurchase program. (See BioWorld Insight, Oct. 5, 2015.)

Even excluding those deals, the total amount of cash raised by the industry would still have broken the existing record.

The turbulent capital markets did serve to slow the public offerings in the fourth quarter, with just $1.3 billion being generated from 22 deals. The top transaction in terms of dollars raised was completed by Kite Pharma Inc., of Santa Monica, Calif., which in December priced an underwritten public offering of about 3.6 million shares of its common stock at $69 per share. Gross proceeds were about $287 million, which included underwriters exercising their full overallotment option, buying an additional 543,650 shares.

As shown in Table 2 the industry typically averages around $4 billion in venture capital annually, or about $1 billion each quarter. In 2015, there was a tsunami of capital flowing to private companies to the tune of $10.3 billion, an amount that establishes a new high-water mark for private financing by the industry.

As shown in Table 2 the industry typically averages around $4 billion in venture capital annually, or about $1 billion each quarter. In 2015, there was a tsunami of capital flowing to private companies to the tune of $10.3 billion, an amount that establishes a new high-water mark for private financing by the industry.

Not surprisingly, private companies enjoyed another highly successful quarter with private global biotechs attracting venture investments that totaled more than $3.1 billion.

Robust Dealflow

Dealflow was robust with companies completing a total of 99 deals.

Interestingly, the number of overseas biotech companies raising private capital has remained steady year over year, according to BioWorld Snapshots data, at around 30 percent.

Among the overseas companies, Taurx Therapeutics Ltd., a company advancing a potentially powerful prodrug of methylthioninium chloride for the potential prevention of neurodegenerative diseases, took top honors in the fourth quarter, closing a $135 million equity financing that will support completion and analysis of phase III trials of the tau aggregation inhibitor, called LMT-X, in Alzheimer's disease and frontotemporal dementia.

The company expects to share top-line data from one of the three ongoing pivotal phase III studies of the drug, also known as TRX-237, during the first half of 2016.

But the standout transaction in the fourth quarter was Cambridge, Mass.-based Boston Pharmaceuticals, which received $600 million in initial funding from the $2 billion health care fund Gurnet Point Capital. (See BioWorld Today, Nov. 20, 2015.)

Humacyte Inc., a biopharma company developing an alternative to current dialysis access products, raised $150 million in a series B preferred stock financing, ranking it as the largest B round of the year, according to BioWorld Snapshots. Research Triangle Park, N.C.-based Humacyte said the new round will support an upcoming global phase III trial of Humacyl, the company's investigational human acellular vessel, being developed to provide vascular access for patients with end-stage renal disease who require hemodialysis. (See BioWorld Today, Oct. 21, 2015.)

Better than expected

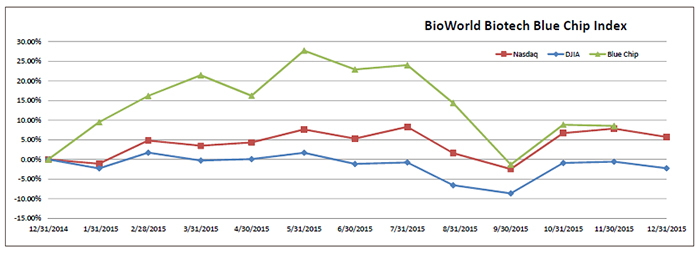

After suffering a 20 percent drop in value during August and September, the BioWorld Blue Chip Biotech Index managed to eke out a 9 percent gain in 2015, a performance thought by many analysts to be out of reach because of the turbulent capital markets that prevailed during most of the second half of the year.

Biotech benefited from a calmer, more positive fourth quarter, with the group recording a more than 10 percent jump in value. Nevertheless, it will be a year that most biotech investors will be glad is over, with the uncertain capital markets that saw the Dow Jones Industrial Average lose more than 2 percent in value in the year. The Nasdaq Composite index closed up 5.7 percent for 2015. (See BioWorld Blue Chip Biotech Index, below.)

For the year, 65 percent of the companies in the group finished in positive territory led by Horizon Pharma plc (NASDAQ:HZNP), whose shares soared 68 percent in 2015 thanks to growing its revenue and acquiring assets through M&A transactions and in-licensing. Its latest deal was in-licensing a series of kinase inhibitors from partner Servier SA in order to refine them for development as personalized medicines, using its genomics discovery research technologies. (See BioWorld Today, Oct. 8, 2015.)

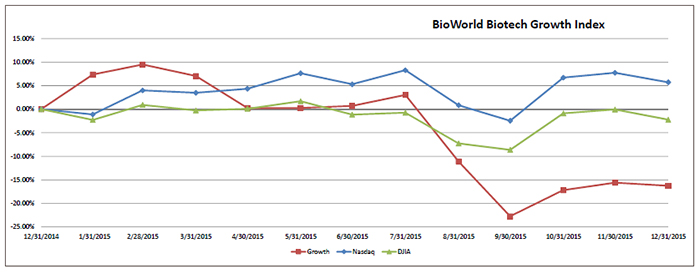

While the large-cap biotech companies managed to weather the capital market turmoil, companies comprising the BioWorld Biotech Growth Index were battered by the unfavorable environment, with the index closing the year with its value down more than 16 percent. (See BioWorld Biotech Growth Index, below.)

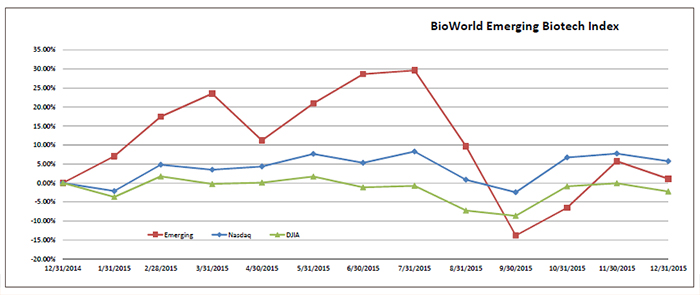

The BioWorld Biotech Emerging Growth Index, which consists of companies that are often subject to wild swings in their share prices, performed remarkably well, closing the year with a modest 1 percent jump in value. (See BioWorld Biotech Emerging Growth Index, below.)

Boosting that group was Otonomy Inc.'s 40 percent jump in its share price for the year on the news that it had received FDA clearance for Otiprio for pediatric patients undergoing ear tube placement surgery. Otiprio, a single-dose, physician-administered antibacterial, is the first-ever cleared for the ear-tube indication in the U.S., and is intended to reduce the rate of treatment failure after the surgery. More than a million tube operations are undertaken every year in the U.S. to deal with recurrent ear infections, with 85 percent of those done in children. (See BioWorld Today, Dec. 14, 2015.)

By the numbers

It was an eventful year for the industry and at its start there were 328 public companies. During the year, 14 were acquired, while 54 new firms graduated to the public ranks. As a result, the industry starts out 2016 with 368 public companies with a collective market cap of $761 billion. At the end of 2015, there were 82 member companies of the billion-dollar market cap club, a 26 percent increase year over year.

Editor's note: The successes and failures of companies during the year necessitates that we rebalance our indices for 2016, and we will be announcing the membership in each group later this month and well as introducing several more focused indices.